Capability-First & Outcome-Driven Enterprise Roadmaps (3/3): Banking and Insurance Simulations

Part 3 of 3: Capability-First & Outcome-Driven Enterprise Roadmaps

- Part 1: Why Most Enterprise Roadmaps Fail Before They Start

- Part 2: The Assessment Blueprint: From Capability Gaps to Transformation Actions

- Part 3: What This Looks Like in Practice: Banking and Insurance Simulations (you are here)

Methodology Is Only as Good as Its Application

In Part 1, we covered why IT-first roadmaps fail and why capability-driven thinking is the fix. In Part 2, we walked through the assessment methodology: three dimensions (criticality, satisfaction, modernization priority), transformation actions, and wave-based journey planning.

Now let’s make it concrete.

This article walks through two industry simulations. Same methodology. Different business contexts. Same dynamics underneath. These aren’t theoretical: they’re composite scenarios drawn from patterns I’ve observed across industries, grounded in real capability hierarchies.

For each simulation, we’ll follow the same structure: business context, capabilities in scope, assessment, transformation actions, and wave-based roadmap.

Simulation 1: Horizon Bank: Post-Merger Digital Transformation

The Business Context

Horizon Bank is a mid-tier ASEAN retail bank. Post-merger, 800+ branches, 10M+ customers, growing fast on digital adoption with 8M+ mobile users. But the legacy core banking platform is holding everything back.

Three strategic goals for the next 3 years:

1/ Grow digital lending share from 15% to 45% of originations. Customers should be able to apply, get approved, and receive funds without stepping into a branch. Today, 80% of loan applications still require manual underwriting.

2/ Unify post-merger customers onto a single platform. Two separate customer databases, two cores, two card platforms. Operational costs are inflated and the customer experience is fragmented.

3/ Expand wealth management. The bank’s wealthier customer segment is underserved. No robo-advisory, no digital wealth platform, no personalized investment recommendations. Competitors are already there.

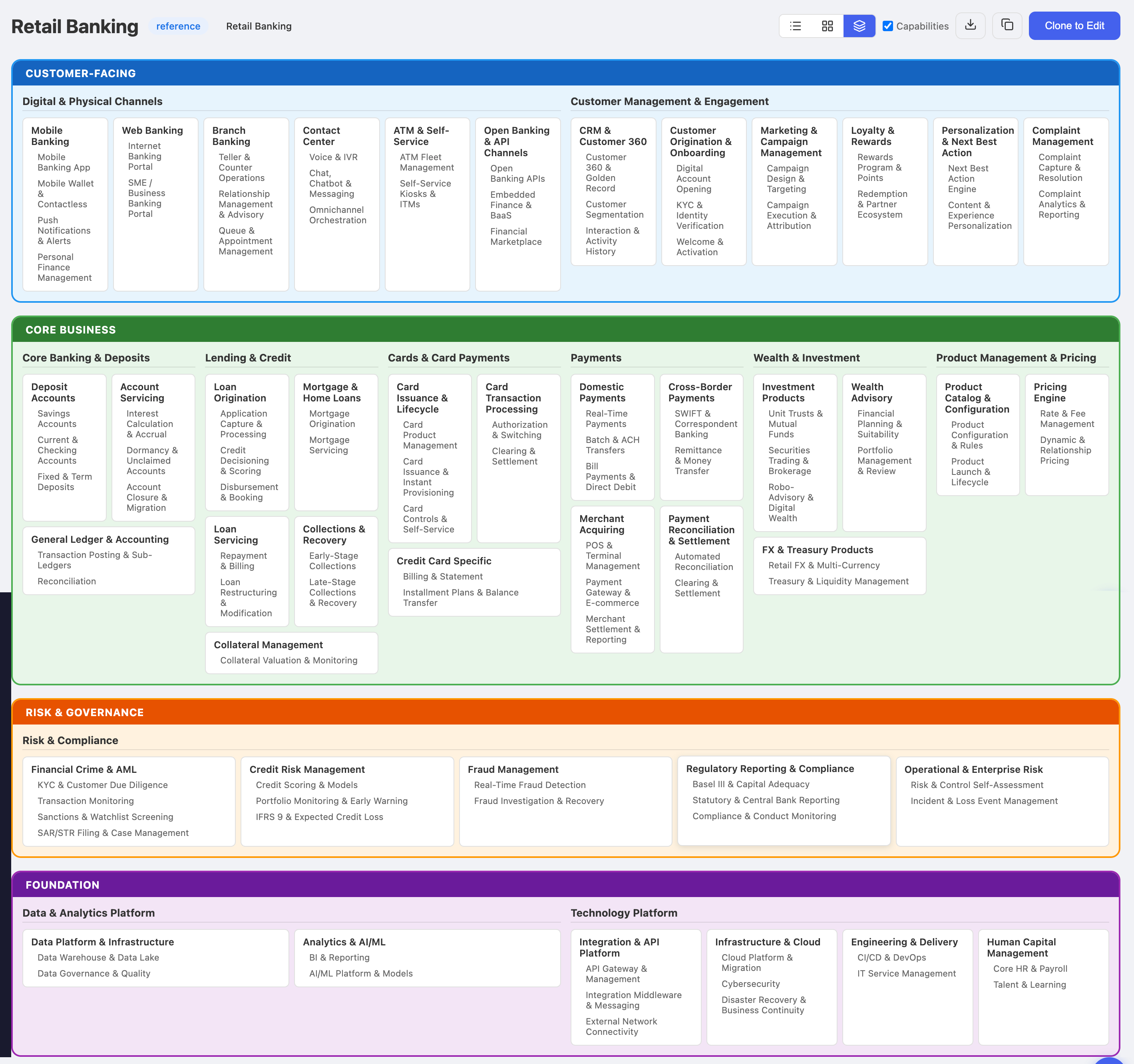

The Capability Map (Retail Banking)

Horizon Bank’s capability model follows the standard retail banking hierarchy: 11 Level 1 capabilities across four domains, expanding to 43 L2 and 105 L3 capabilities that describe what a retail bank actually does.

For this simulation, we’re scoping the assessment to the capabilities that directly serve the three strategic goals. Not the full 105 L3 capabilities, but the 18 that matter most:

| Domain | L1 | L2/L3 Capabilities in Scope |

|---|---|---|

| Customer-Facing | Digital & Physical Channels | Mobile Banking App, Mobile Wallet & Contactless, Internet Banking Portal |

| Customer Management | Customer 360 & Golden Record, Digital Account Opening, KYC & Identity Verification | |

| Core Business | Core Banking & Deposits | Savings & Current Accounts |

| Lending & Credit | Application Capture & Processing, Credit Decisioning & Scoring, Disbursement & Booking | |

| Cards & Card Payments | Card Issuance & Instant Provisioning, Authorization & Switching | |

| Wealth & Investment | Robo-Advisory & Digital Wealth, Financial Planning & Suitability | |

| Foundation | Data & Analytics | Data Warehouse & Data Lake, AI/ML Platform & Models |

| Technology Platform | API Gateway & Management, Cloud Platform & Migration |

The Assessment

Here’s the assessment for each capability in scope. Remember: business criticality is set by business stakeholders, satisfaction comes from the people who live with the capability daily, and modernization priority factors in the strategic context.

| Capability | Criticality | Satisfaction | Priority | Current State |

|---|---|---|---|---|

| Mobile Banking App | High | 4 | Medium | Rebuilt in 2024, native app, 5M MAU. Working well. |

| Mobile Wallet & Contactless | High | 3 | High | QR payments live but on-premises integration. Latency issues. |

| Internet Banking Portal | High | 2 | High | Aging web platform, merger-era dual systems. Poor UX. |

| Customer 360 & Golden Record | High | 2 | High | Two separate customer databases from pre-merger banks. No golden record. |

| Digital Account Opening | High | 2 | High | Online applications start but drop off at 50% due to manual verification. |

| KYC & Identity Verification | High | 2 | High | Manual document review, 3-day turnaround. Bottleneck for everything. |

| Savings & Current Accounts | High | 3 | High | Oracle FLEXCUBE core, dual instances from merger. Needs unification. |

| Application Capture & Processing | High | 2 | High | Paper-heavy. 80% require branch visit or manual follow-up. |

| Credit Decisioning & Scoring | High | 1 | High | 15-year-old custom build. Manual underwriting for most products. |

| Disbursement & Booking | High | 3 | Medium | Works but slow. Average 5-day end-to-end for standard loans. |

| Card Issuance | Medium | 3 | Medium | ACI-based, adequate. Instant provisioning on roadmap. |

| Authorization & Switching | High | 3 | High | Payment switch upgrade needed for real-time interop. |

| Robo-Advisory | Medium | 1 | High | Nothing exists today. Competitors already offer digital wealth. |

| Financial Planning | Medium | 2 | Medium | Basic tools only. No personalization, no suitability engine. |

| Data Warehouse & Data Lake | High | 2 | High | Fragmented, no unified analytics. Two data environments from merger. |

| AI/ML Platform | Medium | 1 | High | No centralized ML platform. Ad hoc models in spreadsheets. |

| API Gateway | High | 2 | High | Limited API layer. Most integrations are point-to-point. |

| Cloud Platform | High | 3 | High | AWS primary, some workloads migrated. Core banking still on-prem. |

Transformation Actions

Based on the assessment, here’s what the transformation plan looks like:

| Capability | Action | Transition Strategy | Rationale |

|---|---|---|---|

| Mobile Banking App | Retain | n/a | High satisfaction, modern stack. Protect the investment. |

| Mobile Wallet | Migrate | Replatform to cloud | On-prem integration causing latency. Move to managed services. |

| Internet Banking Portal | Modernize | Rearchitect | Dual merger systems, poor UX. Rebuild as unified responsive platform. |

| Customer 360 & Golden Record | Modernize | Rearchitect | Two databases must merge into single golden record. Foundation for everything. |

| Digital Account Opening | Modernize | Rearchitect | End-to-end digital with automated KYC integration. |

| KYC & Identity Verification | Build New | SaaS acquisition | Manual process, no system to evolve. Acquire AI-powered digital KYC. |

| Core Banking (Savings/Current) | Migrate | Replatform | Unify dual Oracle FLEXCUBE instances onto single cloud instance. |

| Loan Application Capture | Modernize | Rearchitect | Paper-to-digital transformation. Cloud-native with mobile-first design. |

| Credit Decisioning | Build New | Greenfield | 15-year-old custom build beyond modernization. Build AI credit scoring engine. |

| Disbursement & Booking | Optimize | Process improvement | System works, process is slow. Automate standard product disbursement. |

| Card Issuance | Optimize | Optimize in place | Adequate system. Add instant provisioning capability. |

| Authorization & Switching | Migrate | Replatform | Upgrade payment switch for real-time interoperability. |

| Robo-Advisory | Build New | Build vs. buy | Nothing exists. Evaluate SaaS wealth platforms, build custom only if no fit. |

| Financial Planning | Build New | Greenfield | No adequate system. Build personalized suitability engine with AI. |

| Data Warehouse | Modernize | Rearchitect | Merge two data environments into unified cloud data lake. |

| AI/ML Platform | Build New | Greenfield | No platform exists. Build centralized ML platform on AWS SageMaker. |

| API Gateway | Build New | Greenfield | Replace point-to-point integrations with API-first architecture. |

| Cloud Platform | Migrate | Replatform | Continue cloud migration. Move core banking workloads to AWS. |

The Roadmap: Three Waves

Wave 1: Foundation Modernization (0-12 months)

The merger left Horizon Bank with duplicate systems, fragmented data, and point-to-point integrations. Nothing else on the roadmap works until this is fixed.

| Capability | Action | Business Outcome |

|---|---|---|

| Customer 360 & Golden Record | Modernize | Single customer view across merged entities. Enables personalization. |

| Data Warehouse & Data Lake | Modernize | Unified analytics environment. Foundation for AI/ML. |

| API Gateway & Management | Build New | API-first integration layer. Replaces 200+ point-to-point connections. |

| Cloud Platform & Migration | Migrate | Core banking workloads on AWS. Elastic scaling, reduced infra cost. |

| Core Banking (unify dual instances) | Migrate | Single core platform. Operational cost reduction, simplified operations. |

Wave 2: Core Transformation (12-24 months)

With the foundation stable, transform the capabilities that directly serve the digital lending and channel goals.

| Capability | Action | Business Outcome |

|---|---|---|

| Credit Decisioning & Scoring | Build New | AI-powered credit scoring. 60% of standard loans approved without human intervention. |

| KYC & Identity Verification | Build New | Digital KYC with biometrics. Onboarding drops from 3 days to under 2 hours. |

| Loan Application Capture | Modernize | End-to-end digital application. No branch visit required for standard products. |

| Digital Account Opening | Modernize | Onboarding completion improves from 50% to 80%. |

| Internet Banking Portal | Modernize | Unified portal replacing dual merger systems. Modern UX. |

| Mobile Wallet & Contactless | Migrate | Cloud-based payment integration. Sub-second transaction latency. |

| Authorization & Switching | Migrate | Real-time payment rail ready (InstaPay/PESONet, PayNow, PromptPay). |

Wave 3: Digital and Differentiation (24-36 months)

Build the capabilities that create competitive advantage against neobanks and digital-first challengers.

| Capability | Action | Business Outcome |

|---|---|---|

| Robo-Advisory & Digital Wealth | Build New | Digital wealth platform for mass-affluent segment. New revenue stream. |

| Financial Planning & Suitability | Build New | AI-powered personalized investment recommendations. |

| AI/ML Platform & Models | Build New | Centralized ML platform. Powers credit scoring, fraud detection, personalization. |

| Disbursement & Booking | Optimize | Standard loan disbursement automated. Instant for pre-approved customers, same-day for standard products. |

| Card Issuance & Provisioning | Optimize | Instant digital card provisioning via mobile app. |

Success Metrics

| KPI | Baseline | 12-Month | 36-Month |

|---|---|---|---|

| Digital loan origination share | 15% | 30% | 45% |

| Average loan approval time | 5 days | 48 hours | Same-day (instant for pre-approved) |

| Customer onboarding completion | 50% | 70% | 85%+ |

| Post-merger system unification | 0% | 60% | 100% |

| Wealth management AUM growth | Flat | +10% | +25% |

Notice the difference from Part 1’s failed case study. The ambition is bigger, tripling digital lending share instead of doubling it, but every technology investment is mapped to a specific capability instead of pursued as an end in itself. Cloud migration is part of the solution, but it’s Wave 1 foundation work, not the goal.

Simulation 2: Pacific General Insurance: Claims Modernization and Distribution Digitization

The Business Context

Pacific General is a mid-tier ASEAN general insurer (motor, property, health, travel). The industry is shifting fast: direct-to-consumer channels are growing, embedded insurance via API is becoming table stakes, and customers expect claims settled in days, not weeks.

Three strategic goals for the next 3 years:

1/ Reduce claims settlement time from 45 days to under 10. The current process is paper-heavy, investigation-dependent, and frustrating for customers. NPS on claims is negative.

2/ Launch direct-to-consumer digital channels. Today, 85% of premium comes through agents and brokers. The target: 30% of new policies through digital channels (web, mobile, embedded) within 3 years.

3/ Modernize the core policy administration platform. The legacy policy admin system is 20+ years old, monolithic, and the single biggest bottleneck for product launches. New product development takes 12-18 months. It should take weeks.

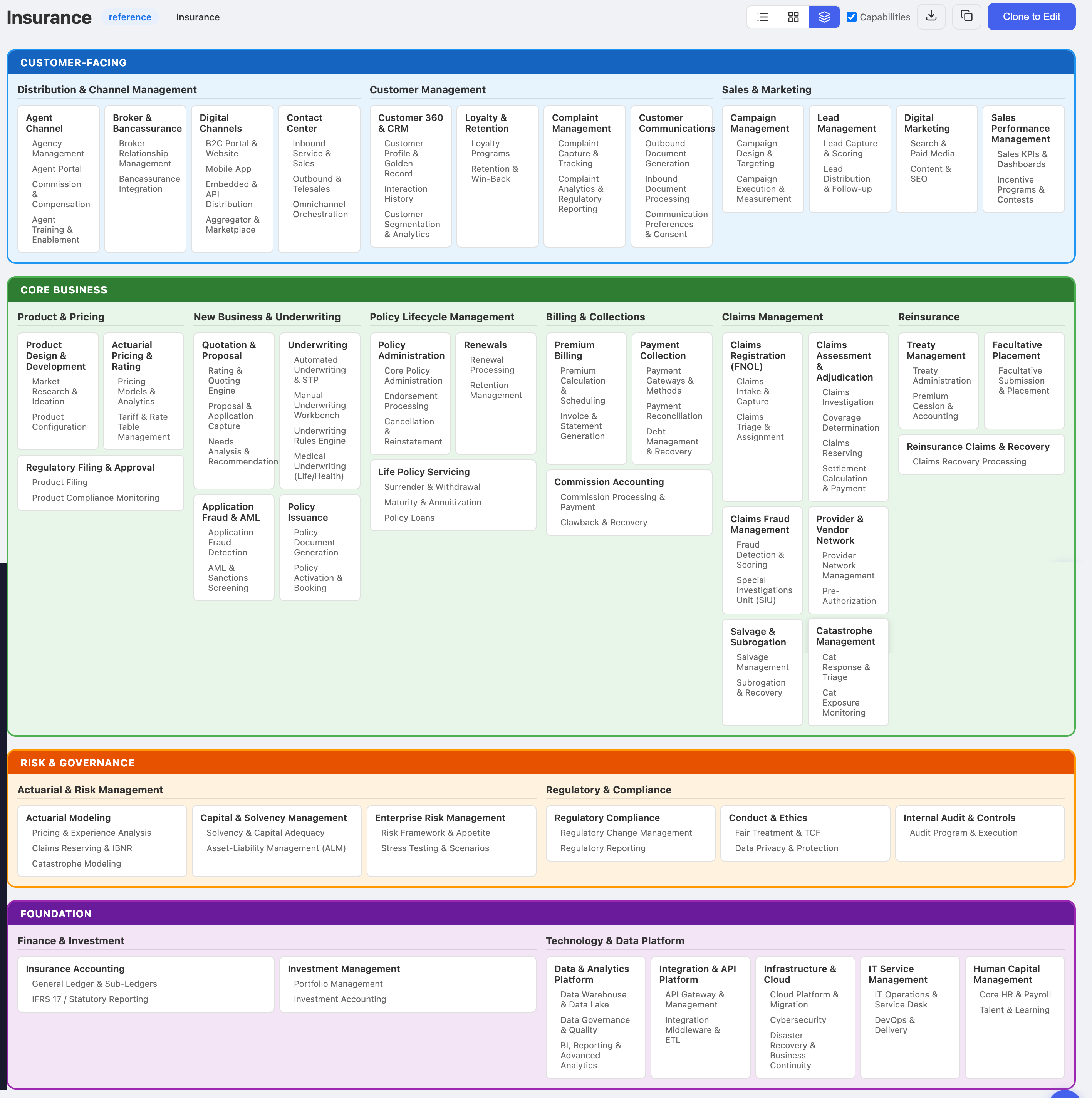

The Capability Map (Insurance)

Insurance capability model: 13 Level 1 capabilities across the same four domains, expanding to roughly 109 L3 capabilities that describe what a general insurer actually does.

For this simulation, we’re scoping to the 23 capabilities that serve the three strategic goals:

| Domain | L1 | L2/L3 Capabilities in Scope |

|---|---|---|

| Customer-Facing | Distribution & Channel Mgmt | B2C Portal & Website, Mobile App, Embedded & API Distribution, Agent Portal |

| Customer Management | Customer 360 & CRM, Customer Communications | |

| Sales & Marketing | Lead Capture & Scoring, Campaign Execution | |

| Core Business | New Business & Underwriting | Rating & Quoting Engine, Automated Underwriting & STP, Policy Document Generation |

| Policy Lifecycle Mgmt | Core Policy Administration, Endorsement Processing, Renewal Processing | |

| Billing & Collections | Premium Calculation & Scheduling, Payment Gateways & Methods | |

| Claims Management | Claims Intake & Capture (FNOL), Claims Investigation, Fraud Detection & Scoring, Settlement Calculation & Payment | |

| Foundation | Technology & Data Platform | API Gateway & Management, Data Warehouse & Data Lake, Cloud Platform & Migration |

The Assessment

| Capability | Criticality | Satisfaction | Priority | Current State |

|---|---|---|---|---|

| B2C Portal & Website | High | 1 | High | Brochure-only website. No online quoting, no policy purchase. |

| Mobile App | High | 1 | High | No customer-facing mobile app exists. |

| Embedded & API Distribution | Medium | 1 | High | No API distribution capability. Competitors already partnering with e-commerce platforms. |

| Agent Portal | High | 3 | Medium | Functional but dated. Agents use workarounds for common tasks. |

| Customer 360 & CRM | High | 2 | High | Fragmented customer data across policy admin, claims, and billing. No single view. |

| Customer Communications | Medium | 2 | Medium | Paper-heavy correspondence. No digital notification system. |

| Lead Capture & Scoring | Medium | 2 | Medium | Manual lead tracking in spreadsheets. No scoring, no automated follow-up. |

| Campaign Execution | Medium | 2 | Medium | Basic email blasts. No segmentation, no measurement. |

| Rating & Quoting Engine | High | 2 | High | Rules hardcoded in policy admin. Takes weeks to change a rate table. |

| Automated Underwriting & STP | High | 1 | High | Almost no straight-through processing. 90%+ of applications require manual review. |

| Policy Document Generation | Medium | 3 | Medium | Template-based, works but slow. |

| Core Policy Administration | High | 1 | High | 20+ year-old monolith. Single biggest bottleneck. Product launch takes 12-18 months. |

| Endorsement Processing | High | 2 | Medium | Manual, error-prone. High rework rate. |

| Renewal Processing | High | 2 | High | Batch-based. No proactive retention. Lapse rate climbing. |

| Premium Calculation & Scheduling | Medium | 3 | Medium | Adequate. Needs digital payment integration. |

| Payment Gateways | Medium | 2 | High | Limited to bank transfer and check. No e-wallet, no card-on-file. |

| FNOL (Claims Intake) | High | 1 | High | Phone and paper only. No digital FNOL. Average 3 days to register a claim. |

| Claims Investigation | High | 2 | High | Manual, field-dependent. No workflow system. Average 30 days investigation. |

| Claims Fraud Detection | High | 1 | High | Rules-based batch processing. Fraud caught too late. Leakage estimated at 8-12%. |

| Settlement & Payment | High | 2 | High | Manual approval chains. Average 45 days FNOL-to-settlement. |

| API Gateway | High | 1 | High | No API layer. All integrations are file-based or direct database calls. |

| Data Warehouse | High | 2 | High | Fragmented. Claims data doesn’t connect to policy data for analytics. |

| Cloud Platform | Medium | 2 | High | Everything on-premises. No cloud adoption yet. |

Transformation Actions

| Capability | Action | Transition Strategy |

|---|---|---|

| B2C Portal & Website | Build New | Greenfield. Digital quoting, binding, and self-service portal. |

| Mobile App | Build New | Greenfield. Customer-facing app for claims, renewals, and policy management. |

| Embedded & API Distribution | Build New | Greenfield. API-first distribution for partner integrations. |

| Agent Portal | Modernize | Rearchitect. Modern UX with real-time policy and claims access. |

| Customer 360 & CRM | Modernize | Rearchitect. Unified customer profile across all systems. |

| Customer Communications | Build New | SaaS acquisition. Digital notification and correspondence platform. |

| Lead Capture & Scoring | Modernize | Rearchitect. Automated lead scoring and routing from digital channels. |

| Campaign Execution | Modernize | Rearchitect. Segmented campaigns with conversion tracking. |

| Rating & Quoting Engine | Build New | Greenfield. Externalized rules engine, configurable by actuarial team. |

| Automated Underwriting & STP | Build New | Greenfield. Rules-based STP engine with ML risk scoring. |

| Core Policy Administration | Modernize | Rearchitect. Phased replacement of monolith with modular policy platform. |

| Endorsement Processing | Modernize | Rearchitect as part of policy admin replacement. |

| Renewal Processing | Modernize | Rearchitect. Automated proactive renewal with retention scoring. |

| Payment Gateways | Build New | SaaS acquisition. Multi-method payment gateway. |

| FNOL (Claims Intake) | Build New | Greenfield. Omnichannel digital FNOL (web, mobile, API). |

| Claims Investigation | Modernize | Rearchitect. Workflow-driven investigation with automated document processing. |

| Claims Fraud Detection | Build New | Greenfield. Real-time ML-powered fraud scoring at FNOL and settlement. |

| Settlement & Payment | Modernize | Rearchitect. Automated approval workflows with straight-through settlement for simple claims. |

| API Gateway | Build New | Greenfield. API-first integration layer. Foundation for all digital channels. |

| Data Warehouse | Modernize | Rearchitect. Cloud data lake connecting policy, claims, and customer data. |

| Cloud Platform | Migrate | Replatform. Cloud-first for all new builds, phased migration for legacy. |

The Roadmap: Three Waves

Wave 1: Foundation and Claims Quick Win (0-12 months)

Two priorities: build the integration and data foundation, and deliver a fast, visible win on claims.

| Capability | Action | Business Outcome |

|---|---|---|

| API Gateway & Management | Build New | API-first integration layer. Prerequisite for digital channels and partner APIs. |

| Data Warehouse & Data Lake | Modernize | Unified claims + policy data. Enables fraud analytics and business intelligence. |

| Cloud Platform | Migrate | Cloud foundation for all new builds. On-premises migration planned for Waves 2-3. |

| FNOL (Claims Intake) | Build New | Digital claims registration via web and phone. Average registration time drops from 3 days to same-day. |

| Claims Fraud Detection | Build New | Real-time fraud scoring at FNOL. Fraud leakage target: under 8%. |

| Customer 360 & CRM | Modernize | Unified customer profile. Foundation for personalization and retention. |

Wave 2: Core Transformation (12-24 months)

With the foundation in place, tackle the two biggest capability gaps: the policy admin monolith and end-to-end claims automation.

| Capability | Action | Business Outcome |

|---|---|---|

| Core Policy Administration | Modernize | Phased replacement of monolith. Product launch time drops from 18 months to 8 weeks. |

| Rating & Quoting Engine | Build New | Actuarial team configures rates directly. No IT dependency for pricing changes. |

| Automated Underwriting & STP | Build New | 70% of standard motor/travel policies issued without manual review. |

| Claims Investigation | Modernize | Workflow-driven, automated document processing. Investigation time: 30 days to 7 days. |

| Settlement & Payment | Modernize | Auto-settlement for simple claims. FNOL-to-settlement: 45 days to under 10 days. |

| Renewal Processing | Modernize | Proactive automated renewals with retention scoring. Lapse rate target: -30%. |

| Payment Gateways | Build New | E-wallet, card-on-file, and digital payment options for premium and claims. |

Wave 3: Digital Distribution (24-36 months)

Build the digital channels that shift the revenue mix from agent-dependent to multi-channel.

| Capability | Action | Business Outcome |

|---|---|---|

| B2C Portal & Website | Build New | Online quoting, binding, and self-service. Target: 15% of new policies via web. |

| Mobile App | Build New | Customer-facing app for claims status, renewals, and policy management. |

| Embedded & API Distribution | Build New | Partner API for embedded insurance. E-commerce, travel, and auto dealer integrations. |

| Agent Portal | Modernize | Modern UX with real-time access. Agent productivity up 25%. |

| Customer Communications | Build New | Digital notifications for claims updates, renewal reminders, and policy documents. |

| Lead Capture & Scoring | Modernize | Automated lead scoring and routing from digital channels. |

| Campaign Execution | Modernize | Segmented campaigns with conversion tracking. |

Success Metrics

| KPI | Baseline | 12-Month | 36-Month |

|---|---|---|---|

| Claims FNOL-to-settlement | 45 days | 20 days | Under 10 days |

| Digital channel policy share | 0% | 5% | 30% |

| Product launch time | 12-18 months | 6 months | Under 8 weeks |

| Claims fraud leakage | 8-12% | Under 8% | Under 5% |

| Underwriting STP rate | <10% | 40% | 70%+ |

| Customer NPS (claims) | Negative | +10 | +30 |

What Both Simulations Have in Common

Strip away the industry-specific details and the same patterns emerge:

Assessment before action. Both roadmaps started with a structured assessment of capability gaps, not a technology shopping list. The three dimensions (criticality, satisfaction, modernization priority) drove every decision.

Foundation first. In both cases, Wave 1 was dominated by data platform, integration layer, and core system work. Not glamorous, not customer-visible, but the prerequisite for everything that follows. Organizations that skip the foundation and jump to digital channels end up building on sand.

Build New where legacy can’t evolve. The toughest decision in both simulations was knowing when a system is beyond modernization. Horizon Bank’s 15-year-old credit decisioning system and Pacific General’s 20-year-old policy admin platform both crossed the threshold: the cost of modernizing exceeded the cost of building new.

Every line item traces to a capability. No orphan technology projects. No “migrate to cloud” as a standalone initiative. Cloud migration appears in both roadmaps, but always as a means to modernize a specific capability, not as the goal itself.

Incentives aligned to outcomes. Success metrics are in business terms: loan approval time, claims settlement days, digital channel share. Not workloads migrated, APIs deployed, or systems decommissioned.

The Challenge

If you’re a CIO, CTO, or enterprise architect reading this, here’s the test:

Pull up your current technology roadmap. For every initiative on it, ask three questions:

1/ What business capability does this serve?

2/ What business outcome does it drive?

3/ How will you measure that outcome?

If you can’t answer those three questions for an initiative, it shouldn’t be on the roadmap. Not because technology doesn’t matter. Because technology without a clear purpose creates complexity, not value.

The roadmap is not a document you produce in Q1 and review in Q4. It’s a continuously evolving strategy that adapts as the business context shifts. The methodology is simple: assess capabilities honestly, decide on transformation actions deliberately, sequence into waves intelligently, and measure in business terms.

The starting point matters more than anything else. Get that right, and the rest follows.

/ Unni